Central Bank of Kenya deputy governor Doctor Haron

Sirima addressing the bankers during the first day of the 14th East

African Banking school hosted by the Kenya Institute of Bankers at

Sarova Whitesands in Mombasa County on Monday 11th August 2014. [Photo/Kelvin Karani]

Central Bank of Kenya deputy governor Doctor Haron

Sirima addressing the bankers during the first day of the 14th East

African Banking school hosted by the Kenya Institute of Bankers at

Sarova Whitesands in Mombasa County on Monday 11th August 2014. [Photo/Kelvin Karani]

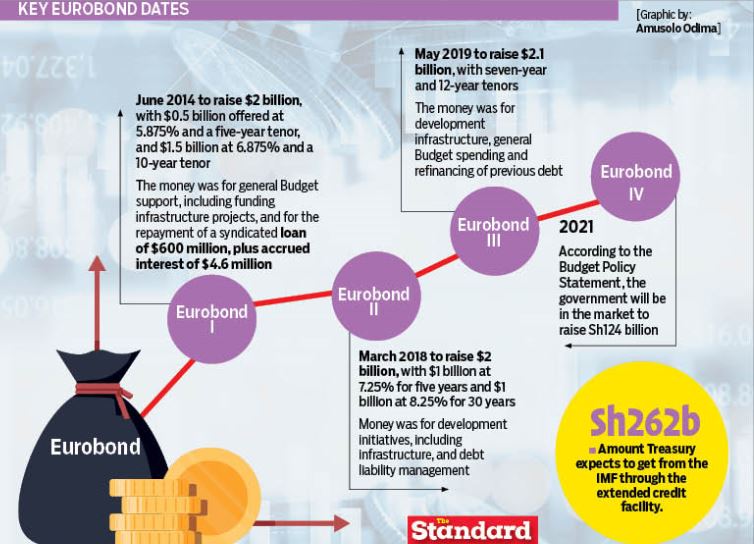

Kenya will return to the Eurobond market to borrow at least Sh124 billion by end of June next year.

This will add to the huge debt burden that has already touched Sh7.3 trillion.

The money will be used to offset part of the principal repayment of Sh351 billion that needs to be refinanced or repaid using borrowed money.

Returning to the international capital markets is Kenya’s Plan B with the National Treasury still hoping to secure cheap loans from multilateral institutions such as the World Bank, International Monetary Fund (IMF) and the African Development Bank.

But with Kenya already having received over Sh500 billion from these institutions, Kenya might be forced to shop for other sources of loans to fund a Sh3.01 trillion budget.

Treasury Cabinet Secretary Ukur Yatani, who was briefing editors yesterday on the possibility of a fourth Eurobond has initially expressed doubts on such expensive loans.

This will be Yatani’s first Eurobond since he took over as the Finance CS in late 2019.

The money will be used to refinance maturing loans - sort of borrowing from Peter to pay Paul.

Haron Sirima, the Director-General for Public Debt Management Office

at the National Treasury confirmed that the country had to access the

“international capital market to refinance some of the large debt

maturities” in what is aimed at minimising debt service costs. Key Eurobond dates. [Graphics: The Standard]

Key Eurobond dates. [Graphics: The Standard]

Like the earlier Eurobond loans, the money will also be used for both budgetary support and repaying expensive loans that will be falling due.

He insisted that they would only dive into the Eurobond market should Kenya fail to get concessional funding.

Sirima noted that the rules of the market do not allow an issuer to reveal the money they want to raise or when they intend to issue the bond as this might skew the market. However, in the Budget Policy Statement of 2021-22, the National Treasury notes that it expects disbursement of a sovereign bond worth Sh124.3 billion in the financial year ending June next year.

This will push Kenya’s stock of Eurobond cash to Sh734 billion.

So far, Kenya has borrowed about Sh610 billion from the Eurobond or a sovereign bond that is denominated in dollars.

Kenya will also not participate in the restructuring of private debts, a sign that it wants to retain a good credit rating which is critical for creditors.

External debt repayment in the next financial year is estimated at Sh613.4 billion, with the Treasury expected to refinance more than half of this.

Since the State cannot repay all these loans from its tax coffers, it expects to refinance principal payments of close to Sh351 billion.

In addition to the Sh262 billion that the National Treasury expects to receive from the IMF through the extended credit facility, Kenya also expects the Washington-based institution to wire Sh54 billion to the Rapid Credit Facility.

Kenya could use some of the money from the IMF to refinance expensive maturing loans.

Moreover, Treasury is also keen to get Sh74 billion loan from the World Bank’s development policy operation, which it can also use to refinance its debts.

The other loans that Treasury will receive are mostly project and programme loans that have already been planned for.

In the financial year ending June next year, Kenya’s budget deficit, including grants, is estimated at Sh930 billion.

This budget deficit will be plugged through net external borrowing of Sh267.3 billion and net domestic borrowing of Sh662.8 billion.

Expensive loans

Since Kenya became a low middle-income country, it has relied a lot on expensive loans after taps for cheap loans closed.

However, these loans have come at a higher cost with the debt service costs growing faster than income.

As a result, the IMF and the World Bank have downgraded Kenya’s risk of debt distress to low.

This follows the adverse effects of the Covid-19 that affected export earnings.

By the time the current administration leaves office next year, it will hand over a debt burden of Sh10 trillion to the next regime - beyond the Sh9 trillion legal ceiling.

When Yatani took over as Treasury CS, he vowed to stay away from expensive loans and implored ministries to tighten their belts, so as to keep the country’s debt sustainable.

But the pandemic scuttled his austerity plans, dragging the country back into a borrowing frenzy.

No comments :

Post a Comment