Picture: 123RF/SCANRAIL

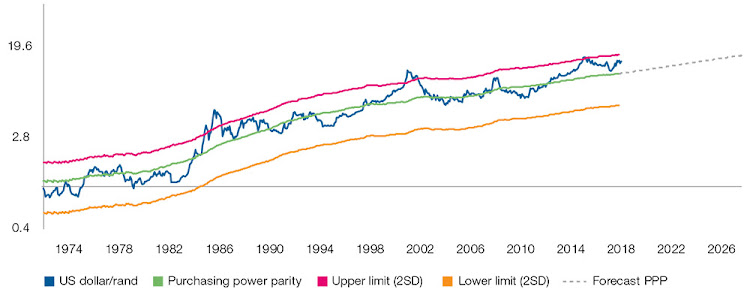

Figure 1: US dollar/rand purchasing power

parity. Picture: I-Net Bridge, Bloomberg and Investec Asset Management

as at 11.12.18, Log Scale.

About the author: Paul Hutchinson is sales manager at Investec Asset Management. Picture: SUPPLIED

The impact of exchange-rate risk on a foreign investment should also be an important consideration.

Many South Africans got burnt when they invested offshore in 2001 and 2002 when the rand traded at around R12 to the US dollar. As a result, South African investors now tend to have an underweight exposure to foreign investments.

Studies have shown that when considering the historical returns of foreign investments, the impact of the exchange rate is uncertain and volatile, and that when measured over shorter periods, the exchange rate can have a significant impact on the investment return in rand.

Research indicates it is only over longer periods that the underlying investment contributes more to the return than the exchange rate. Therefore, Investec Asset Management is of the opinion that when investing offshore, investors need to take a long-term view to fully benefit from the return potential of the international assets in which they are invested.

No comments:

Post a Comment